MBCC Trading Highlights 16th November'22 - when everything moves in the same direction so fast, it is a BLOW OUT, not fundamental...

We have said time and again that bear markets can have nasty squeezes, at the risk of not finding another word to depict just how violent the moves/pnl can be during these times. These markets are the hardest to trade and even bearish traders lose out if positions are not sized correctly and portfolio levered. As often what tends to happen is that one is right but has to endure quite a bit of pnl pain in between. Hence the Hedge Fund leverage model of 6:1 times never works as one is stopped out in a few days. Only to see the moves reverse at the top and come back into play. This is why we recommend easing into our calls and risk managing, i.e. getting the time exactly right is work of the divine, we are but humble portfolio mangers. But yes, managing risk is essential and timing the entry/exit and averaging into it is crucial. Our aim is to survive the moves and capitalise on blow out moves as Prop desks/Hedge Funds have no choice as they get the call from upstairs, no matter their conviction, the bank always has a much bigger agenda.

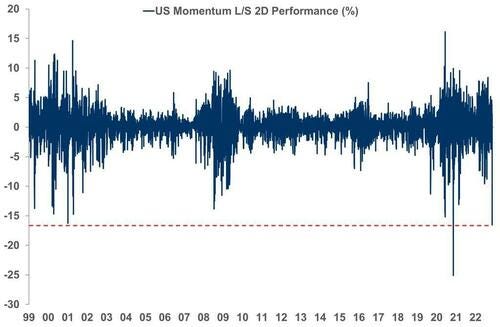

Going back tot he markets, just to show you how violent the move of the last week has been, see chart above showing the stunning chart from Morgan Stanley according to which high-momentum L/S funds had just suffered their 2nd worst 2-Day drop in the past 20 years! These are NOT normal markets as moves like this DO NOT MEAN the start of a new trend, in fact, it is a blow up, and like 2008 and other crisis, there will be quite a few before the market bottoms.

We explain why the derivative positioning is such that the S&P 500 will be pinned at 4000 and capped above that. Of course tons of factors point to that as well, but do not underestimate the power of gamma hedging. As that influenced the move in QQQ 0.00%↑ as well. It is all one big macro trade and quite technical especially when you have long/short funds trying to find some sense in the moves as well.